Unpacking the “Unexpected” January Jobs Report

If you’ve been following the economic tea leaves like I have for over 30 years in this game, you know the drill: Wall Street “experts” cluster their forecasts like sheep, the media slaps “unexpectedly” on anything that doesn’t fit their narrative, and real-world metrics get buried under a pile of revisions and spin. Today’s January 2026 BLS jobs report? It’s a classic case. Clocking in at +130,000 nonfarm payrolls with unemployment ticking down to 4.3%, this thing smashed the lowball consensus and kicked off the year with a bang for the Trump administration and Republicans. And yeah, it’s leading national news cycles as a “strong start”-but don’t hold your breath for the qualifiers to fade. That “unexpectedly” hedge? It’s been a useful cover since the Obama years, and it’s out in full force today.

January’s job number came in higher than 78/80 economists in Bloomberg’s survey predicted.

— Geiger Capital (@Geiger_Capital) February 11, 2026

Let’s start with the forecast miss: experts versus cold, hard reality. The consensus from Bloomberg, Reuters, and Dow Jones hovered in that pessimistic 55k–80k range, with big names like Bank of America and Goldman Sachs dialing it down to around +45k. They baked in the gloom from those brutal 2025 revisions, which slashed the year’s total job growth to a measly 181k (about 15k per month average). With my decades watching these cycles, it’s the same old song: Forecasters herd together on the low side, revisions rewrite history downward later, and when a beat like this lands, it’s spun as a “surprise” to cover the collective whiff. No wonder the markets perked up-reality trumps echo chambers every time.

Speaking of proprietary data debacles, take Bank of America’s internal deposit-based payroll tracker. Their early February report flashed green: a +0.8% year-over-year rebound in paycheck inflows, stabilizing unemployment claims at around 9% YoY growth, and hints of “re-acceleration” in the labor market. Sounds promising, right? But then their public forecast leaned hard pessimistic, pegging the headline at ~+45k with underlying growth around 75k excluding revisions. That fed right into the low consensus that made the actual +130k look like a blockbuster. Sure, their data offers some useful breakdowns-like after-tax wage growth stratified by income (higher earners at +3.7% YoY, middle at +1.6%, lower at +0.9%)-but as a predictor of the BLS print? About as valuable as the price of tea in China when the official numbers diverge. I’ve seen these bank models flop too many times; they hedge their bets while the real data does the talking.

Remember Margaret Thatcher’s wisdom whenever they talk about diverging income levels.

Now, onto the real metric that counts: wages beating inflation. Average hourly earnings for private nonfarm workers hit $37.17 in January, up 0.4% month-over-month and a solid 3.7% year-over-year. Stack that against the latest CPI at ~2.7% for December 2025 (January figures drop in a couple days), and you’ve got about a 1 percentage point gap in positive real wage growth. This strikes directly at affordability-the everyday squeeze on households from groceries to gas. When wages outpace inflation, purchasing power climbs, consumer spending gets a lift, and life feels less like a grind after those high-inflation years. Sure, it’s not uniform across income tiers, but the aggregate trend is a clear win for working folks, often overshadowed by the media’s fixation on revisions or that “unexpected” framing. In communities just like mine across America this means more breathing room for families amid local growth in construction and services.

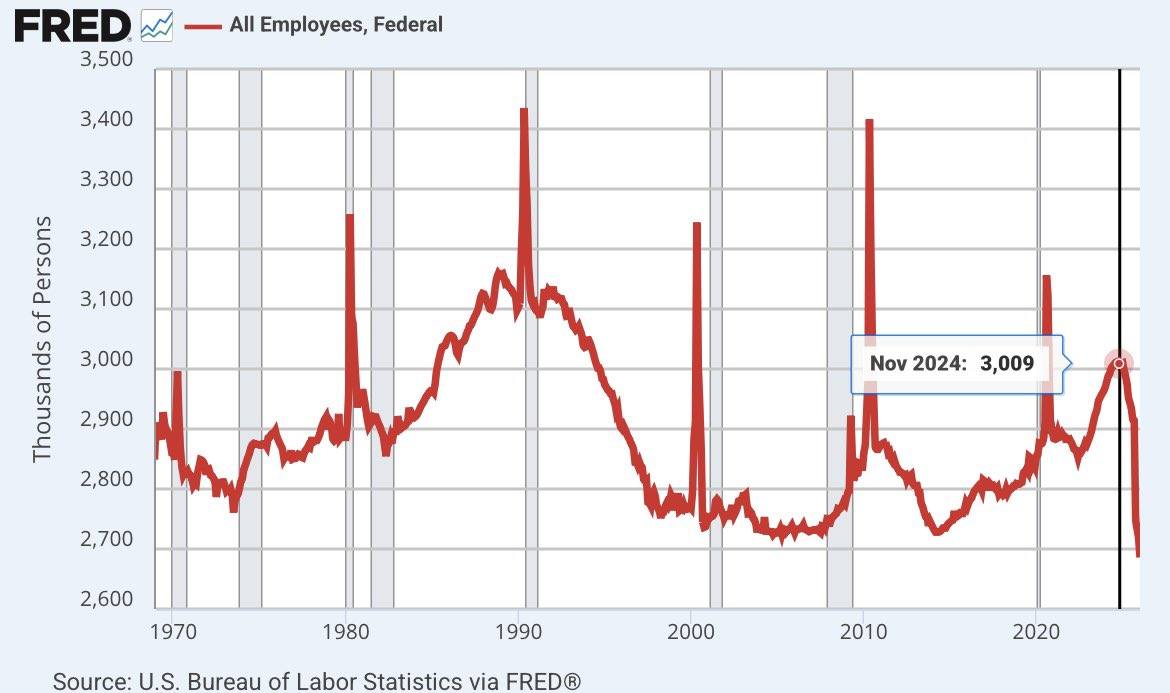

And let’s not gloss over the federal jobs declining. January saw a -34,000 drop in federal government employment, partly from deferred resignations tied to 2025 retention offers finally hitting payrolls. Broader picture? That’s down 327,000 jobs-or 10.9%-since the October 2024 peak, pushing federal levels to their lowest since the 1960s in some measures. This isn’t some accidental drag; it’s intentional policy from the Trump team and the Department of Government Efficiency (DOGE), slashing unelected bureaucracy and freeing up resources. It offsets some softness elsewhere while keeping overall nonfarm positive, thanks to robust private-sector adds at +172k. This FRED chart shows the sharp drop from 3,009k in November 2024 onward, which is a strike against the Deep State. With my long view, this is reform at work: trimming the bloated administrative state aligns with smaller-government principles and lets the real economy thrive.

And let’s not gloss over the federal jobs declining. January saw a -34,000 drop in federal government employment, partly from deferred resignations tied to 2025 retention offers finally hitting payrolls. Broader picture? That’s down 327,000 jobs-or 10.9%-since the October 2024 peak, pushing federal levels to their lowest since the 1960s in some measures. This isn’t some accidental drag; it’s intentional policy from the Trump team and the Department of Government Efficiency (DOGE), slashing unelected bureaucracy and freeing up resources. It offsets some softness elsewhere while keeping overall nonfarm positive, thanks to robust private-sector adds at +172k. This FRED chart shows the sharp drop from 3,009k in November 2024 onward, which is a strike against the Deep State. With my long view, this is reform at work: trimming the bloated administrative state aligns with smaller-government principles and lets the real economy thrive.

Then there’s the Fed’s big miss: holding rates despite the momentum. Jerome Powell’s crew paused at the January 28 FOMC meeting, keeping the federal funds rate steady in the 3.5%–3.75% range after three quarter-point cuts late last year. This came amid Trump’s vocal push for deeper easing-maybe even down to 1% or below-to slash government debt costs and supercharge growth. Powell justified it with talk of a “firm footing,” stabilizing labor, and “somewhat elevated” inflation (nodding to tariffs), insisting on a data-dependent, meeting-by-meeting vibe without admitting policy’s restrictiveness. Two Trump appointees dissented for a cut, but the majority held. Post-jobs report? Markets shoved cut bets out to mid-2026, with the strong print affirming “Fed patience” but underscoring a missed chance to amplify Trump’s policies. Those reforms-deregulation, infrastructure, federal trims-are thriving despite the drag of artificially high rates, delivering private gains, real wages, and bureaucracy cuts. The economy’s resilient in spite of this Keynesian overcaution, but easing now could’ve turned good into great. With Powell’s term up in May and a potential successor like Kevin Warsh waiting, this institutional whiff might not last-but it’s costing upside in the meantime.

Broader implications for 2026 and the administration? This January surge-led by health care, social assistance, and construction-pairs with real wage gains and bureaucracy reduction for policy-aligned momentum after 2025’s weakness. Sectors like services hold firm, and the Fed’s likely to stay on hold longer, but a new chair post-May could pivot things dovish. Watch the media and institutional patterns: If these positives get downplayed amid “unexpected” spin or cautionary tales, it fits the decades of bias I’ve tracked. But the data? It screams recovery and reform under Trump.

Bottom line: Ditch the consensus hype, proprietary models, and Fed caution-prioritize the durable BLS realities like real wages, private-sector strength, and federal trims over expert echoes. Cycles evolve, trends rise and fall, but my skepticism of groupthink, media hedges, proprietary spin, and institutional misses never goes out of style because style is timeless, but fashion’s only now. The Fed’s hold ranks as the biggest recent forecast whiff in my book-how does it stack up against the misses you’ve spotted from past eras? Drop your thoughts on X @James_K_Bishop.