A Bold Path Forward for GOP Healthcare Reform Through Reconciliation

Republicans in the House and Senate, the clock is ticking louder than ever. With the Affordable Care Act’s enhanced premium tax credits poised to expire on December 31, millions of Americans face premium doublings—from an average of $888 to $1,904 annually for subsidized plans according to one study by the Kaiser Family Foundation—potentially spiking uninsured rates by 4 million in 2026 alone. Democrats are already gearing up to blame us, with polls showing 48% of voters pointing fingers at the GOP and 76% of marketplace enrollees ready to hold us accountable if chaos ensues. But here’s the truth: This impending “subsidy cliff” isn’t a trap—it’s our golden opportunity to deliver transformative reform.

After the Senate’s procedural defeat on the Health Care Freedom for Patients Act (S. 3386)—failing cloture 51-48 despite a strong show of Republican unity for the core idea—we cannot afford to let this moment slip. I beseech you: Rally now for a second reconciliation bill. Harness the filibuster-proof power of budget reconciliation to pass bold, market-driven changes with just 51 votes. This isn’t timid tinkering; it’s a chance to dismantle Obamacare’s inefficiencies, empower patients, and tackle the root costs driving our healthcare crisis. Heading into the 2026 midterms, such audacity will galvanize our base, shield vulnerable members in swing districts, and prove to independents that we’re the party of real solutions—not endless bailouts.

Let’s synthesize the wealth of GOP proposals we’ve developed—from Speaker Mike Johnson’s House conference slide to Sens. Bill Cassidy and Mike Crapo’s Senate HSA bill—and forge them into a cohesive reconciliation package. These aren’t abstract ideas; they’re battle-tested reforms rooted in conservative principles of competition, personal responsibility, and fiscal restraint. By weaving them together, we can create a system where patients, not bureaucrats or insurers, hold the reins—decoupling coverage from jobs, fostering portability, and bending the cost curve downward for generations.

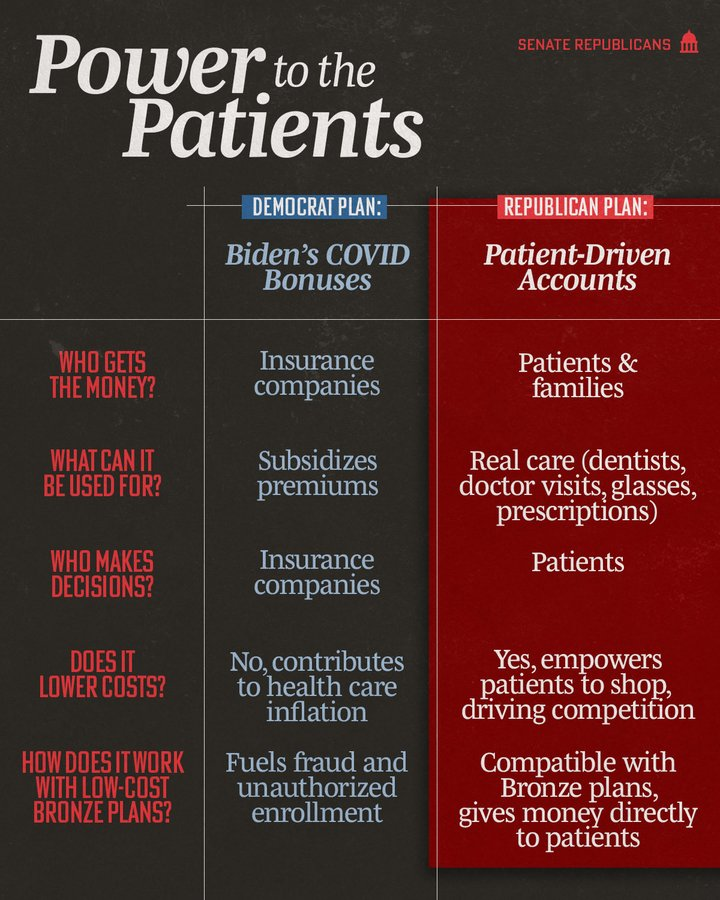

Start with the Senate’s flagship: The Health Care Freedom for Patients Act redirects the $26 billion slated for 2026 enhanced premium tax credits away from insurer pockets and into pre-funded Health Savings Accounts (HSAs) for eligible marketplace enrollees. The details reveal its elegance: U.S. citizens on bronze or catastrophic ACA plans (with incomes up to 700% of the federal poverty level—about $218,050 for a family of four) would receive monthly deposits of $1,000 annually for ages 18-49 or $1,500 for ages 50-64.

Start with the Senate’s flagship: The Health Care Freedom for Patients Act redirects the $26 billion slated for 2026 enhanced premium tax credits away from insurer pockets and into pre-funded Health Savings Accounts (HSAs) for eligible marketplace enrollees. The details reveal its elegance: U.S. citizens on bronze or catastrophic ACA plans (with incomes up to 700% of the federal poverty level—about $218,050 for a family of four) would receive monthly deposits of $1,000 annually for ages 18-49 or $1,500 for ages 50-64.

These funds cover out-of-pocket expenses like deductibles, copays, prescriptions, dental visits, glasses, and even wellness items if prescribed—bypassing insurer overhead (which siphons off up to 20% of subsidies). Paired with cost-sharing reductions (CSRs) for low-income enrollees (up to 250% FPL), it promises premium reductions exceeding 10% through stabilized markets and competition. This isn’t a handout; it’s empowerment—encouraging patients to shop for value, where cash payments can slash service costs by 50-70%. And it’s fiscally neutral in year one, with long-term savings projected at $30 billion federally by shifting burdens from taxpayers to informed consumers. Boldly, this bill also includes anti-fraud safeguards, like a $25 monthly minimum contribution to deter improper enrollments, addressing the GAO’s damning findings of $27 billion in waste from fake applications and overused SSNs.

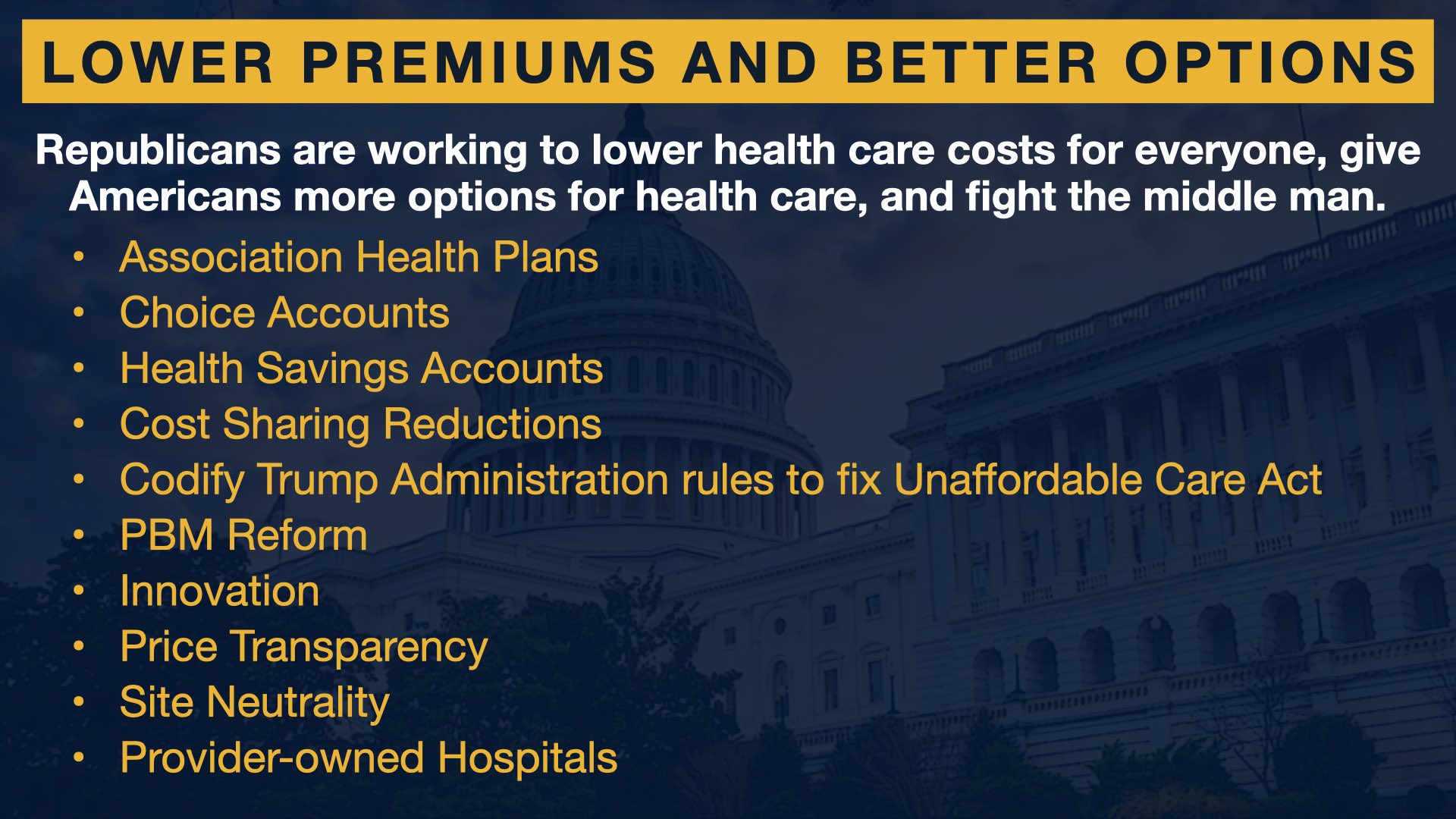

Now, amplify this with the House’s comprehensive 10-option menu from Johnson’s slide, which targets intermediaries and inefficiencies head-on.

Let’s examine each for clarity and urgency:

- Association Health Plans (AHPs): Allow small businesses, self-employed individuals, and associations to band together for group purchasing power, bypassing some ACA mandates. This could save healthy groups 10-20% on premiums by pooling risks and negotiating like large employers, expanding options for entrepreneurs and fostering competition without government overreach.

- Choice Accounts: Expand Health Reimbursement Arrangements (HRAs) so employers fund employee-chosen individual plans tax-free, promoting flexibility and reducing administrative burdens.

- Health Savings Accounts (HSAs): Build on the Senate bill by raising contribution limits (from $4,300 self/$8,550 family in 2025), allowing fitness expenses (up to $1,000), and pairing with more plan types like direct primary care—creating triple-tax-advantaged savings that roll over indefinitely for true portability.

- Cost-Sharing Reductions (CSRs): Fund federal payments to insurers for low-income deductibles and copays (up to 250% FPL), stabilizing markets and reimbursing costs without deficit spikes—directly lowering out-of-pocket burdens for vulnerable groups.

- Codify Trump Administration Rules: Make permanent expansions like short-term plans (up to 12 months, 50-80% cheaper than ACA options) and transparency requirements, offering flexible, low-mandate coverage that promotes choice and innovation.

- PBM Reform: Regulate pharmacy benefit managers by delinking fees from drug prices and requiring rebates pass to patients—potentially saving billions annually by fighting middlemen profiteering, a bipartisan win with real impact on prescription costs.

- Innovation: Deregulate to accelerate FDA approvals, telemedicine, and models like direct primary care, reducing barriers and fostering breakthroughs that lower long-term expenses through efficiency and new technologies.

- Price Transparency: Enforce upfront disclosure of prices by providers and insurers, empowering consumers to shop and potentially cutting costs 10-20%—building on Trump-era rules with stronger compliance to demystify billing.

- Site Neutrality: Equalize Medicare payments for services regardless of venue (e.g., hospital vs. clinic), ending inflated hospital reimbursements and saving $150-200 billion over 10 years—directly combating consolidation that jacks up prices 12-14%.

- Provider-Owned Hospitals: Lift the ACA moratorium on new physician-owned facilities, boosting competition and allowing doctors more control while preventing “cherry-picking” through safeguards.

To turbocharge competition and choice, incorporate a long-standing GOP priority: Changing the law to allow health insurance to be sold across state lines. This reform, freshly revived by Sen. Marsha Blackburn (R-TN) in her Health Coverage Across State Lines Act introduced this week, would permit insurers to sell policies nationwide while adhering primarily to their home state’s regulations—eliminating the patchwork of state-specific mandates that currently fragment the market and inflate costs. Details highlight its potential: By enabling companies to bypass costly requirements in high-regulation states (e.g., mandates for acupuncture or infertility treatments that add 9-23% to premiums), healthier consumers could access cheaper plans from less-regulated jurisdictions, potentially driving down overall prices through interstate competition.

Blackburn’s rationale is crystal clear—empower Americans to choose tailored coverage without being trapped in overpriced local monopolies, breaking up insurer dominance and expanding options for small businesses and individuals. This echoes complementary proposals, like Sen. Rick Scott’s (R-FL) November 2025 bill combining interstate sales with HSA options for ACA plans, and Sen. Rand Paul’s (R-KY) measure allowing large corporations like Costco or Amazon to negotiate group insurance for employees, further amplifying collective bargaining power. While critics warn of a “race to the bottom” with skimpy plans, real-world evidence from pre-ACA experiments shows it could foster innovation without eroding core protections—especially if paired with safeguards like network adequacy requirements. In reconciliation, this fits as a revenue-neutral deregulation with indirect budgetary impacts through lower federal subsidies over time, making it a Byrd Rule survivor and a bold strike against Obamacare’s silos.

These aren’t fillers; they’re expository blueprints for systemic overhaul. By incorporating them into reconciliation—where budgetary elements like spending reallocations and tax advantages qualify under the Byrd Rule—we sidestep filibusters and Democratic obstruction. Precedents abound: Our summer 2025 reconciliation bill (H.R. 1) navigated the “Byrd Bath” to advance HSA expansions like retroactive contributions and telehealth eligibility, even after stripping non-fiscal items. S. 3386’s core—PTC redirection and CSR funding—fits perfectly, as do anti-fraud tweaks and Medicaid matching rate reductions for non-qualified benefits.

To supercharge portability, integrate Individual Coverage Health Reimbursement Arrangements (ICHRAs): Employers of any size fund tax-free reimbursements for employees’ individual market plans, with no contribution caps and rollovers for unused funds. This decouples benefits from jobs—ideal for gig workers and remote staff—while maintaining ACA protections like essential benefits and pre-existing condition coverage. Adoption surged 34% among large employers in 2025, proving its appeal for budget control and inclusivity.

House and Senate Republicans, I implore you: Launch this second reconciliation bill immediately. Craft a new budget resolution by mid-January, directing committees to refine this package—focusing on fiscal impacts to survive Parliamentarian scrutiny. Don’t fear the naysayers; Trump’s endorsement of “direct to people” gives us the wind at our backs, and base voices demand we nuke the filibuster mentality and act; reconciliation gives us the means to do it. This is bold conservatism: Patient-driven HSAs and ICHRAs foster empowerment, while structural fixes like site-neutrality and PBM reform attack root costs—consolidation, drugs, and admin waste—that premiums merely reflect.

In the 2026 midterms, voters won’t reward timidity. They’ll celebrate leaders who halved Obamacare’s burdens, saved trillions long-term, and put power back in families’ hands. Be the party that fixes the mess Democrats created—not the one that lets it fester. Seize reconciliation, reform healthcare, and secure our majorities. The American people—and history—will thank you.